In the current market volatility, investors are looking for options to earn a safe rate of interest and protect their capital. Here’s a quick overview of RBI Bonds vs Tax Free Bonds vs Target Maturity Funds. This should help you pick one of these if you need to.

A comparison – RBI Bonds vs Tax Free Bonds vs Target Maturity Funds

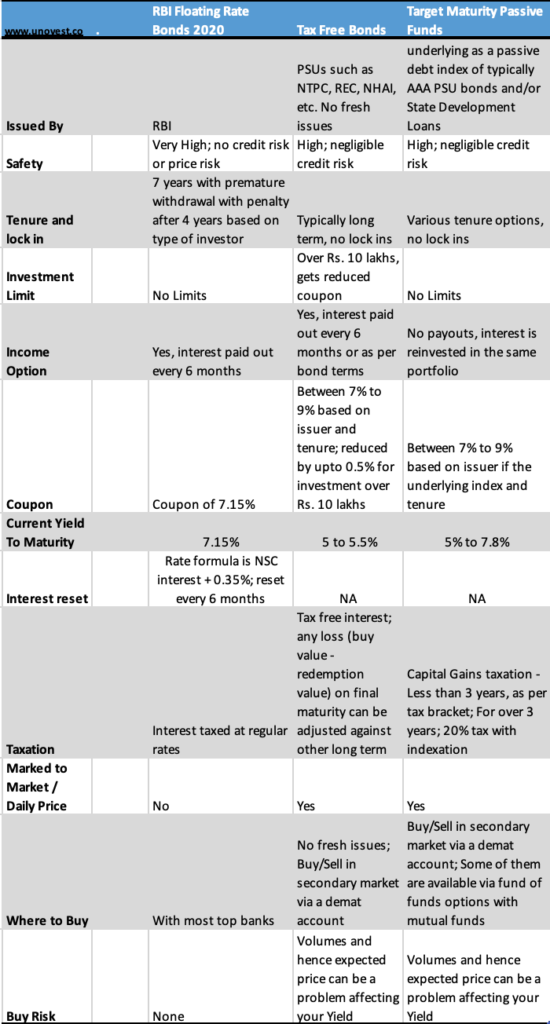

RBI Floating Rate Bonds 2020

- Issued by RBI, no credit risk

- No limit on investment

- Interest rate set at NSC + 0.35%, current interest rate of 7.15%, taxable (with 30% tax, post tax about 5%

- Interest reset every 6 months (can go up as bond yields go up)

- Interest payout every 6 months (TDS applicable)

- Bond tenure is 7 years with an option to exit with penalty after 4 years

- Can be bought through most large banks

- No mark to market or price risk

Tax Free Bonds

- Available from top PSUs such as PFC, NHAI, IRFC, REC, etc. for maturities of 2025, 2027, 2030, 2031, 2035, etc.

- Current net of tax yield to maturity around 5.5% (coupon rates can be higher but yields to maturity matter)

- interest paid out half yearly/yearly basis, no TDS

- For amounts over Rs. 10 lakhs, coupon rate is reduced (0.5% lower in case of REC and 0.25% lower in case of NTPC) and hence yield can go down upto 5%

- Marked to market with a daily price; Important to hold the bond till maturity else indicative yield may not be realised

- Have to be bought in the secondary market in a demat account.

- Buy Price is important for the yield. Volumes can be low and hence the right price to realise the yield may not be available, thus lowering the yield.

- No lock ins

Passive Target Maturity Funds

- Target maturity funds which invest in State Development Loans / PSU bonds, etc. Typically, Low credit risk

- Examples, Bharat Bond April 2032 with current yield at 7.8%

- No interest payouts; all interest received by the fund is reinvested

- More tax efficient as long term capital gains of 20% post indexation applies after 3 years (much like debt funds)

- Marked to market with a daily price; if you sell before maturity, the expected gains may not accrue because of price fluctuations.

- ETFs Bought in the secondary market via demat account, the fund of fund option (which doesn’t require a demat account) charges an extra expense

- No lock ins

So, what do you do?

These investments are high on safety. However, most of them are long term options and hence keep that in mind.

Yields have already inched up and some of the tax free bonds as well as Target maturity funds are available at attractive YTMs.

RBI bonds are probably the simplest way to take a risk free, income paying investment with a similar yield as tax free bonds (specially if you have to invest over Rs. 10 lakh).

Passive debt funds are more tax efficient don’t pay out interest. They grow in value. Beyond your EPF, PPF, SSY, Bank FDs, they can be useful as Asset Allocation components on the bond /fixed income side.

The RBI RetailDirect Platform too has some options with a higher yields currently. I am exploring the platform and shall write about it soon.

Leave a Reply