I have worked for 17 years in the financial industry, more specifically, investments. Even more specific – Mutual Funds.

I was better placed to understand the investment world. But must admit that it did not save me from committing some stupid mistakes.

In fact, contrary to the popular perception, most of the people from the industry succumb to their overconfidence and make the worst of mistakes.

I have been no exception.

Over the years, I have got calls from friends, family and relatives asking for advice.

They presume “He knows”. Nothing could be farther from the truth.

Yes, I can claim to have the knowledge but more as a burden. I have had my own journey replete with same concerns and biases as any other common investor does.

The only redeeming thing so far is that I could rise above them. Here’s a short account of how it all went.

I would like to talk about my investing journey in this article and will do it in following three parts:

- The Journey

- The Method

- The Learnings

#1 The Journey

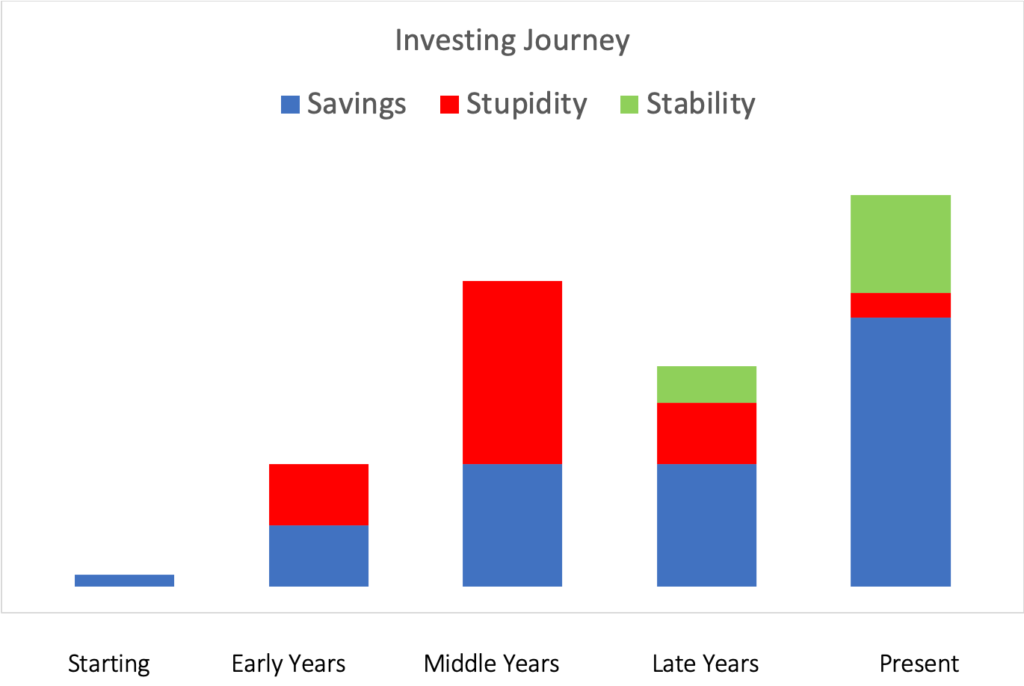

I can visualize my investing journey over time as interactions between the following elements: Savings, Stupidity, and Stability.

Savings – we all know what it implies;

Stupidity – I don’t mean as mistakes but mistakes in the process of decision making and not in the decision itself.

When I started my career I had small savings, which I invested in 2-3 equity mutual funds. It turned out to be a good decision not by choice but by the situation. The reason was the amount to invest was too small and confidence to try something fancy was absent.

I was lucky that my career started at an insurance company. It was a brief one and, very importantly, the one that seeded the first thoughts of “what not to do with your money”.

I could figure out early the importance of plain term insurance and the criminality of mixing insurance with investment.

As I moved on to the early years of my career and heard smart fund managers my confidence to try something fancy grew.

Though I still had small amounts of savings, I started trying new things and introduced the element of stupid in my portfolio.

It was stupid as the only objective of the investment was to increase wealth as fast as I can with a limited understanding of what I was getting into.

Thanks to the influence of some illuminating fund managers, I took that risk on limited savings.

The thing about rash investing is that if you are unlucky you will get some quick returns initially, which increases your confidence and your size of bets – only to lose it all. (Pray you are unlucky with such decisions!)

Going back to the Savings, Stupidity, Stability chart, you can see that in the Late Years, the overall length of the bar is lower than the middle years. This is because I did lose money in a few shares and MFs, after making good returns initially.

That was when I was blessed with some good investing lessons and the little green bar (Stability) started showing up.

The stability was not in terms of returns but in terms of my mental framework towards investing. I realized that one needs to have patience, realistic expectations, and a proper approach towards investing basis one’s attitude and understanding.

That position was developed a few years ago and currently, it has only strengthened from where I was. The latest bar is high both on savings and stability.

Let me iterate, the stability is about my approach to investing decisions within a framework.

As I write, 90% plus of my portfolio is into a small portfolio of stocks and the balance in liquid / ultra-short-term funds. But it’s stable in terms of my investment philosophy which is a high conviction concentrated portfolio of 10 to 15 stocks.

A BarBell Approach

Today my portfolio is demarcated between two types of investments – Wealth Creation and Capital Preservation

Wealth Creation is for my long-term goal of building wealth with the help of equity. I know it is volatile but has a good probability of helping me achieve my financial goals over the long run. By long run, I refer to my whole investing life wherein there would be points wherein I would need money, at other points invest more, but mostly, I would just be sitting tight.

Capital Preservation: This is the safest possible basket comprising of liquid fixed income options such as Liquid Funds, Ultra Short-Term Funds, and Bank Deposits for the following objectives

- Emergency funds

- Specific near-term purpose

- Temporary parking of surplus

The other good options are RBI Bonds, KVP, etc if somebody is ok with locking away the money.

I have absolutely no interest in investing in high-yielding deposits, credit risk funds, P2P lending, covered bonds, insurance, or any such fancy product for the probability of few extra basis points in returns.

I have also added protection through plain vanilla Term Insurance, which covers my financial dependents.

I never mix what is for wealth creation, capital preservation, and protection.

Side Note> You will have to lot of smartly tied executives or pretty ones from Banks offering you the best of mocktails/cocktails of the 3 and claim it as “God’s gift to mankind”. You listen to them but never buy. To me, every such ‘NO’ keeps the stupidity bar further away.

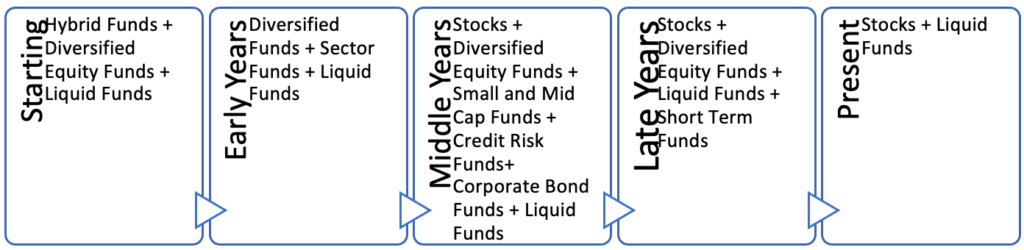

Glimpse of my portfolio composition over 17 years

My portfolio today is very concentrated and volatile with just 5 stocks making up 75% of the portfolio but I still call it stable as it is an outcome of a conscious strategy – I understand the risk, have reasonable expectations, and willing to accept a range of outcomes for my investing approach.

Last year my portfolio went down by more than 40% in the Covid induced aftermath but it had ZERO impact on my sleep. Of course, nobody other than a Sadist will want their portfolio to go down but not wanting is one thing and knowing it can happen is another. Not just I did not lose a single day of sleep over the portfolio going down, I was instead thinking about investing more (if I had the money).

Finally, if you see the investing journey chart it still shows some red even in present, that is to account for the unknown unknowns. As I move on, I will make some mistakes, some of which may have to be labelled as stupidity.

#2 The Method

So, the madness in early years did help in creating a method.

At this stage my investing philosophy is “High Conviction Concentrated Stock Portfolio” with following principles

- Invest for the long term, run full course in wealth creation journey of a company

- Bias towards smaller companies with strong balance sheets and honest management

- Sit through occasional setbacks and don’t mistake volatility for risk

- Accept that some companies are going to be duds in the portfolio and many multi-baggers would be outside of my portfolio

- Need just a handful of stocks for the lifetime of wealth creation

- Take benefit of being an individual investor

- Ignore the acquisition price for any sell decision

Outsource research to the experts and don’t follow more than 2 to 3 advisors/fund managers

#3 The Learnings – Yes, I drop a few pearls of wisdom I have learnt

- Loose Vanity, Not Sanity

- I invest to make money and not to feed my ego. It’s ok if I don’t own the hottest fads of the day. I am willing to stay quiet in room where everyone is talking about bitcoin but won’t let that come in way of money making more money

- Averaging down is a bottomless pit

- Have lost more money just to average down my buying price, it truly is like catching a falling knife

- Forget about buying price while making a sell decision

- Once I have bought a share the only reason I will sell whenever it will be solely dependent upon prospects in which the price paid to acquire is meaningless information at best, and at worst, something which could lead to decision paralysis.

- Don’t come into the way of compounding by selling too soon

- The only reason a stock should be sold is if you need money for something or if it has diminished prospects. We tend to cut the compounding story short by booking profits when the stocks go up by 50% or 100% or so. Just let it be.

- Portfolio Sizing

- Need to invest a significant part of the portfolio in each security. Otherwise, its impact on the total wealth may be irrelevant.

- Don’t Panic But Do Prepare

- Panic amplifies the problem at hand. It usually happens when we don’t understand what we have invested in or are not willing to accept the outcome. Once we understand what we are getting into it is critical to prepare for the possibility of downturns and unfavourable outcomes. Having low fixed expenses and a fair amount of emergency savings is one of the ways to prepare for it

- Return Per Unit of Stress

- Peter Lynch one said the right body organ to understand your risk appetite is the stomach. If your stomach ache’s while you have investment is going through a volatile period, it’s trying to tell you something

- No Regret Investing

- This is where the search for the holy grail ends – I hope to reach eventually the stage of No Regret Investing – not because of the outcome of investing but on the conviction on my process and acceptance of any investing outcome.

- Being in control

- There are only two options either we are in control or are being controlled. I’ll let you ponder over where you are on this aspect of investing.

It goes without saying that this is my journey, my experience, my learnings, my investing – it may or may not fit someone else – we don’t want Bed of Procrustes here.

And as Yogi Berra said,

It ain’t over till it’s over

When we meet next time who knows the bars on the investing journey chart may look much different as we would have benefit of hindsight at that time.

This is a guest post by Ashish Sethiya, a learning machine and who carries a healthy disregard for everything.

Nice post. Why such a concentration of 5 stocks? Can it not be 10 to 15 especially the aim in late years is to “preserve” rather than “high growth”? I know there are no right oror wrong answers here, but to keen to know your insights.

The concentration has happened over time as he built conviction in the portfolio.

The way the experiential process evolved for this conscienscious investor is very instructive learning and focuses on how one should groom himself without being entangled in what one reads, listens,. Better to listen, read, enrich knowledge, but, be yourself in taking investment decisions.

I have done my long journey as banker, in different domains, still journeying in my sun setting years ; an octogenarian.

Mutual fund exposure being my last lap of journey, when NSE was just born when I ended my career journey, that last twinkle of knowledge enabled me to be in the process of learning as much as I could . Learning by incremental investing ; it’s going on. I have my own share of mistakes to learn more . To me technicals is exotic, but, fundamentals are the wherewithal , even if I make mistakes. My hind sight made me avoid mutual funds in my portfolio. I would like someone’s mistakes to impact my portfolio. Fund Mangers make all the difference in that cutting edge performance. But, they are not bonded or committed to one Fund. They move on with price- tags. I wanted to be my own, notwithstanding aging. At this point I settled to investing not to enjoy wealth , but, leave behind a diversified portfolio for my inheritors, but in the process remain mentally agile . I agree that core part of portfolio could be limited number of under ten for better balancing and floating number should be very limited so that the benefits of core not neutralised.

Good luck to all investors.

My hearty congrats to the author of this article who made me read hearfully.

Drk

Admirable style.Salut