An investor believes that his/her dharma is to get more returns and every single penny should chase the maximum returns possible.

Heck, if it means choosing a short term debt fund for doing an STP over a liquid fund, so be it.

Well, it might just work for a few investors. For most others, it is the other way round.

Saving more beats chasing returns.

I worked a simple example to bring this to light, again.

Who wants to be a Crorepati?

Let’s say you are out there to get your first Rs 1 crore as soon as possible. That is your only goal, the only way to feel rich.

You have no savings today but you are about to put all your energies chasing that 1 crore.

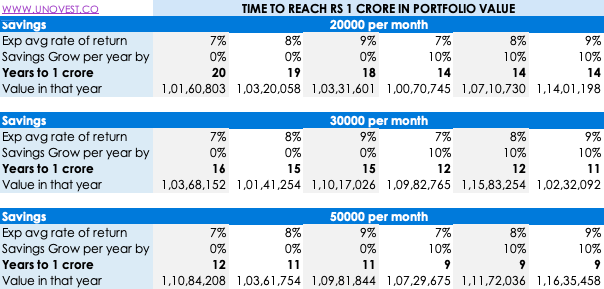

As your advisor, I have listed the likely scenarios that you can choose from (see image below)

If you choose to invest Rs. 20,000 per month with a higher rate of return of 9% (50:50 equity:debt portfolio), you will touch Rs. 1 crore in portfolio value only in the 18th year.

However, if you work with just a 7% return and ensure that you are able to increase your savings by 10% every year, the crorepati tag awaits you in the 14th year itself.

Which one is a safer and more certain way?

I know it is not easy to wrap our heads around it. Our mistaken dharma about choosing winning, high return investments will always make us question a lower but certain return.

For some reason, chasing that alpha is what makes us feel alive and yet:

“More money has been lost reaching for yield than at the point of a gun.”

Raymond DeVoe Jr.

Let’s dig into the choices further.

If you were to save Rs. 30,000 per month and ensure that your savings grow by 10% every year, the difference in time to reach that 1 crores is just a few months here or there, across return paths.

And yet, which is a safer and more certain way?

You are not holding it against me for the extra lakhs that the returns produce, are you? 🙂

The lesson to me is clear – Saving More trumps Chasing returns!

What about you?

Read More:

Leave a Reply