As I plan to increase my insurance cover, I evaluate one of the most popular term plans out there – HDFC Life Click2Protect 3D. Well, turns out that the good old simple term insurance now comes with a lot of bells and whistles. If you don’t know what you want, you can end up paying extra premium unnecessarily.

I bought the original Click2Protect many years ago. But now that I evaluate it again, I am not sure how useful are these bells and whistles?

I set out to do a detailed analysis of this plan and see what makes sense and what does not. Hopefully it helps you too.

What does 3D stand for in CLick2Protect 3D?

No, you are not getting free 3D glasses!

The 3Ds stand for Death, Disability and Disease. (The country is undergoing an acronym overload.)

Death is the most important provision of a life insurance policy. In case of death, the insurance company pays out the Sum Assured under the policy to the dependents/nominees. Suicide too is covered after 12 months of policy existence.

There is an additional built in provision for Terminal Illness too. If 2 certified doctors given an opinion in writing that the life insured has a terminal illness and can survive a maximum of 6 months survival, the sum assured is paid out to you. Terminal illness excludes HIV/AIDS.

Disability covers loss of income due to total permanent disability only. Loss of 2 or more limbs / parts, as defined by the policy.

Note: The policy already has a built in waiver of premium benefit in case of permanent total disability. No need to pay anything extra for it.

Disease here refers to critical illness. The policy provides a lumpsum benefit in case of detection of 19 critical illnesses, as defined under the policy.

#1D – Death Benefit

This is the most important part of any life insurance policy. You select the amount of insurance cover. I am looking to buy Rs. 1 crore cover policy.

When you choose the Base Sum Assured, there are several other bells and whistles, also called Add Ons, which you can add to your policy. Let’s take a quick look at them.

- Top up of policy benefits – You can increase the Base Sum Assured and other benefits under the policy from 0.1% to 10% every year.

- Waiver of premium due to critical illness – On detection of any of the 34 listed critical illnesses, all your future premiums will be waived off.

- Accidental Death Cover – If death takes place due to accident, then an additional sum assured is paid out. You choose the amount at the time of buying the policy.

- Income Replacement Benefit – over & above the Death Benefit OR just the income replacement. The premium payable is higher for income over & above the death benefit.

- Return of Premium (ROP)- If you survive the policy tenure and end up making no claim, you will get a refund of all your premiums paid.

The top up benefit is mainly about ensuring that your insurance cover remains relevant to costs and changing needs of your dependents. A 10% annual increase in insurance cover can be good, but remember that it also increases your premium every year. The increase in benefit is logically followed by an increase in costs. In my experience, if you are under 30, you might find the need to increase your premium, however, in the 40s, as you gather assets and build wealth, the need for a life insurance cover may go down. It can vary from case to case. I am not going for this add on.

The Waiver of Premium due to critical illness seems to be a reasonable benefit and it comes at a very low cost too. I will go for it.

The Accidental Death Cover option is redundant too. If I am planning my life insurance, I want to work it on the primary truth that I might not live and my dependents need money. Now, I die because of an accident or a disease, is not in my control. I would plan my base sum assured to account for all eventualities. No need of this add on too.

The Income Replacement Benefit is one of the reasons I want my insurance cover, but I don’t my insurance company to do this for me. I prefer that my family gets the lumpsum benefit and it decides how best to use it for any goals or to meet expenses.

The ROP or return of premium is the most ridiculous add on available. It more than doubles the premium amount. Basically, you are paying them up more money to return your premiums in the future, the absolute amount, without any increase / growth. You take ROP option only when you don’t understand the concept of insurance. As is obvious, I am not taking it.

#2D – Disability Benefit

You can opt for an additional sum assured for Disability Benefit. With this benefit, if 2 of your limbs/parts are permanently disabled, then the policy pays out 1% per month of the Sum Assured under this benefit for 10 years.

So, if I add another Rs. 1 crores under Disability Benefit then on the occurrence of the event, I will be paid Rs. 1 lakh per month for 10 years.

Unfortunately, this is the only benefit under Disability cover and makes it look very deficient.

Typically, if you were to go for a stand alone accident and disability policy, you get a lumpsum payout of the Sum Assured in case of Total Permanent Disability. In case of Total Temporary Disability, you get paid a weekly / monthly income benefit.

Hence, the disability benefit under Click2Protect 3D is not worth opting for.

#3D – Disease or Critical Illness Benefit

Under this benefit, the policy pays out a separate Sum Assured as defined for this option. The benefit clicks in after 90 days of policy issuance. You have to survive for at least 30 days before you can make a claim under this option. Remember, only 19 critical illnesses are covered under this benefit. (Yes, the waiver benefit enjoys a bigger list!)

It is a fact that as individuals, we are underinsured for health covers. A Critical illness treatment can burn a big hole in your pocket. IN that scenario, this option can make sense.

Compared to stand alone critical illness policy offered by HDFC Ergo, which offers max Rs. 10 lakh Sum Assured, the rider with HDFC Click2Protect 3D is more generous. With a one crore base cover, I can opt for Rs. 25 lakhs Critical Illness benefit.

Now look at it another way. If you have adequate health insurance cover say of Rs 30 to Rs. 50 lakhs, you are protected for treatment costs for almost all kinds of illnesses and treatments. With an adequate life cover, your family gets the required money, that is, in case of death. Overall, the Critical Illness policy option becomes useless. Now, you may want to skip this option too.

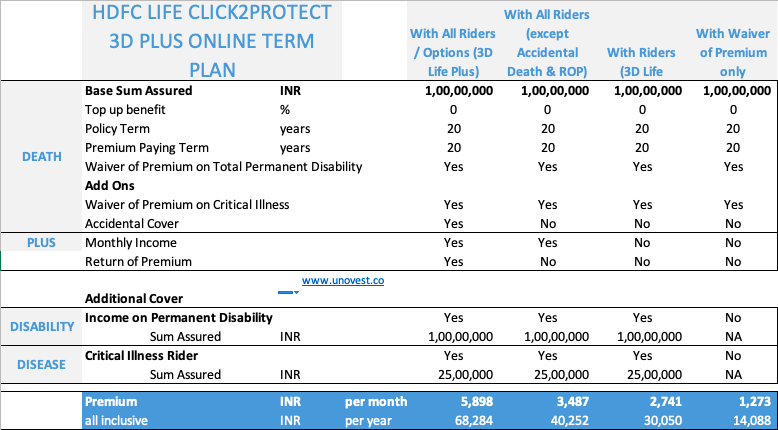

Comparison of premium with various options of Click2Protect 3D

Source: HDFC Life online. The above calculations are for a male, age 39.

From the 3Ds, Disease or Critical Illness is the biggest contributor of premium. In the Add Ons, the return of premium (ROP) option almost doubles the premium (taking from one hand to give to the other).

As you can notice, if you choose the right and relevant options, you can save a lot of money. Unless, you are an HDFC Life shareholder, this extra premium is effectively money down the drain.

Well, I am going for the basic life cover with waiver of premium option (the last column).

What are you likely to do?

Why not go for ICICI PRUDENTIAL I PROTECT SMART

Sure,if it is fits your requirements.

But coverage is for 20 years only..do hdfc have 80 year’s coverage?

Why would you need an 80 year coverage?

Aegon Life has cover till 100 years along with Critical Illness cover till 80 years. And the premium rates are way lower.

I would like to pen down my personal exp of something similar with actual exp of what hdf life can do inspite of issuing a policy on its own unilateral decision. Its all mafia inclduing the notorious gang co worker policy bazaar.

Please do share it in detail. It will be of great help to everyone.

Surprisingly, just saw the date of your above note. It coincides with the days when i was duped in and issued soemthing which was later withdrawn and told.me to settle with less..polic bazar vanished on being challeneged.

It’s good, but not all information is correct,

Coz there’s difference between 3D plus & 3D life option,

Most of the person get confus between 3D & Critical illness Rider,

It’s better way to buy this policy form consultant,

They will guide each and everything about plan option.

My son age about 30 year you have any life insurance policy for 20 year sum assured less 5 lacs and premium come for 1 year

Yes it will be there, but not in Term Insuranceplan you have to buy another plan

where as Hdfc gives till 99yrs with till 85ys critical illness coverage

One needs to review the fine print and understand the administrative changes that will be levied on a monthly basis.

The resultant will leave u shocked!!!

I applied for policy and paid premium in 10th April 20 hdfc life got the mesg today on 26th September 20 that policy has been issued will hdfc give intrest cost benefit of premium amount paid 6 month back when I applied there was no medical requirement but after making payments they ask for medical

Documents after documents

Not completely online process

U can file ITR with aadhe based otp why it cant be used in policy